Taxes rarely make for exciting reading material, but if you own an investment property, there’s at least one set of IRS regulations you absolutely will want to understand: 1031 Exchange Rules. Why? Because normally when you sell an investment property for more than what you paid for it, you’d have to pay a hefty capital gains tax.

But with a 1031 Exchange, you get to defer paying those taxes if you reinvest the proceeds in a new property, making an “exchange” rather than a sale. You are able to leverage funds otherwise needed to pay capital gains taxes to acquire more desirable property. As the name implies, a 1031 Exchange is a swap of one investment property for a like-kind property instead of a traditional sale.

Property owners may exchange real estate held for investment for another property of like-kind and so long as the properties are held for investment, all real estate is deemed to be like-kind. If the transaction qualifies, any realized capital gains are deferred until the replacement property is sold at a later date. Many investors would like to do a 1031 exchange. Some of them who do fix and flip call us for a 1031 exchange to roll the gain over into the next property. But can they?

Although confusing, understanding IRS Code Section 1031 is worth it. It’s just that this transaction is subject to some strict regulations, so you’ll need to follow the 1031 exchange rules to the letter. For example, an exchange can only be made with like-kind properties, and IRS rules limit use with vacation properties. Another common misconception is that property sold in a particular state must be replaced by a property in the same state.

But that’s not true as the “like-kind” requirement is very general and allows for the property owner to acquire property outside of his state should they wish to do so. However, some complications can arise where multiple states are involved. For example, California has a “clawback” requirement for California investment property sold in a 1031 exchange and subsequently replaced with a non-California investment property per California FTB Publication 1100 Irev 2007, section F.

Any capital gains accrued on California real estate will be subject to California tax upon the ultimate sale of the real property even if the investor had sold his or her California real estate and subsequently 1031 Exchanged into investment property located outside of California. Therefore, if the replacement property is out-of-state, California aggressively tracks when the replacement is ultimately sold.

When the replacement property is sold, California treats the gain as California source income to the extent of the original deferred gain. That is so even if you no longer live in California and if you are selling the non-California property twenty years later. Several other states follow this rule, but California may be the most aggressive in enforcing it. So what’s the drawback?

The “clawback” provision can affect you negatively when you try to exchange out of California’s stringent tax system into a friendlier state tax system such as Nevada or Texas as both of these have no state income tax. Here’s all the more you need to understand and execute a 1031 Exchange process successfully in 2021.

What is a 1031 Exchange?

A 1031 Exchange is an incredibly useful tool for many real estate investors. It is an exchange of two (or more) pieces of real estate under Section 1031 of the tax code. A simple definition of 1031 exchange properties is the property being sold and the property being purchased under Section 1031 of the tax code. In the simplest case, you’re swapping one property for another.

Internal Revenue Code Section 1031 allows individuals and entities to “exchange” investment property or other property that is held for productive use in a business or trade but not primarily for sale. The IRS Code Section 1.1031 states that no gain or loss is recognized if property held for productive use in a trade or business or for investment is exchanged solely for property of a like kind to be held either for productive use in a trade or business or for investment.

The important words are are property and held. “Property” refers to real property while “held” means the time when the property is used in productive use of a business or investment. The shorter the time held, the greater the facts need to be to substantiate that the property is used for the proper intent rather than for a flip or for profit. Properties that do not come under 1031 consideration include primary residence, inventory, partnership interests, indebtedness, stocks, securities, and notes.

1031 exchnage can come with high legal fees and strict limits. However, this is often worth it, given the great benefits of a 1031 exchange. This explains why the 1031 exchange is used by businesses to “move up” in buildings, selling their existing ones to buy a larger facility with minimal taxes. Although, a 1031 exchange process is complex it is one of the best tax advantages real estate investors have at their disposal.

There are several initial steps to a successful 1031 exchange process. For example, you’ll want to find a qualified intermediary before you sell the property. Then there is the process of listing the property you want to sell. The first step in the 1031 exchange is selling the first property. It is advisable to have potential replacement properties identified at this point.

However, you don’t have to close on these properties immediately. If the 1031 exchange properties cannot be closed simultaneously, the money must be held by a qualified intermediary. This means the taxpayer doesn’t receive the money from the sale of the first property.

The second step in a 1031 exchange is formally identifying your replacement property. This must be done within 45 days of the sale date of the first property. Ideally, you’d have begun the purchase process.

The third step of the 1031 exchange process is to complete the purchase of the replacement process including payment and retitling of the property. The facilitator will hold the cash from the sale of the first property and send it to the seller of the replacement property. Then the 1031 exchange is treated as a swap by the IRS and considered done once you fill out the IRS form.

In general, you have 180 days from start to finish. However, you may have to do so even faster. For example, you generally have to complete the process before you file your tax return claiming the 1031 exchange. This means you’ll want to complete the 1031 exchange started last tax year before you file your tax return the following April.

If you actually acquire the replacement property before the first one sells, this is called a reverse exchange. The property must be held by an exchange accommodation titleholder. This could be a qualified intermediary. You’ll get the title transferred to you when the first property sells.

What happens if there is money left-over after the new property has been purchased? Maybe the new property costs less than you expected after all costs are taken into account. Or you didn’t use all of the money toward the purchase of a new property. A tax penalty will be owed, but it is typically only for the amount that wasn’t rolled over into the new property.

What Are The Types of 1031 Exchanges?

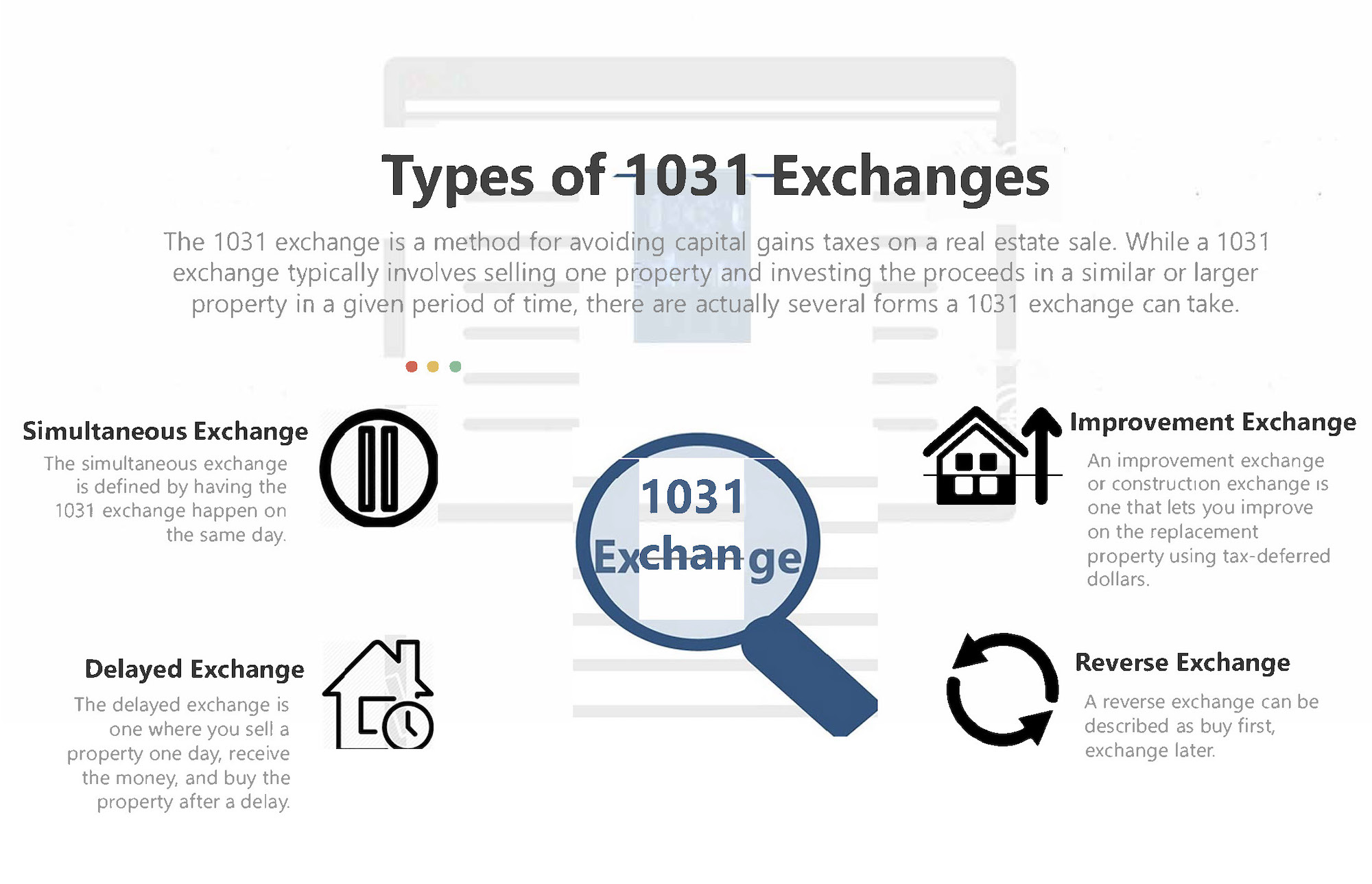

Simultaneous 1031 Exchange

The simultaneous exchange is defined by having the 1031 exchange happen on the same day. It was also the original form of the 1031 exchange until updates to tax law made the others possible. There are several ways the simultaneous exchange may happen. You might have a two-party trade.

In this case, two parties literally exchange or swap deeds. In a three-party exchange, an accommodating party facilitates the exchange by transferring ownership between the parties so they close on the same day. Another option is using a qualified intermediary who handles the entire exchange.

Delayed 1031 Exchange

The delayed exchange is one where you sell a property one day, receive the money, and buy the property after a delay. It could be anywhere from one day to several months before acquiring the replacement property. If you don’t buy replacement property within the time limits set by the IRS, you will have to pay capital gains on the proceeds from the original property sale. The money from the initial sale must be held by a third party “exchange intermediary”.

This third party may also be called a Single Purpose Entity. The 180-day time limit starts the day you execute the sale and purchase agreement for the first property. However, you have 45 days to identify a new piece of real estate and you have 180 days to complete the transaction. Fortunately, this gives you several months to negotiate the purchase price, arrange for the seller to make repairs, and perform a proper title search.

Improvement 1031 Exchange

An improvement exchange or construction exchange is one that lets you improve on the replacement property using tax-deferred dollars, though the money is held by a qualified intermediary. There are several requirements you must meet if you want to defer all of the gains from the sale of the relinquished property.

First, all of the exchange equity must be used as either a down payment on the new property or spent on completed improvements. You’ll run into problems if the work isn’t completed within 180 days. And remember that this 180-day time frame includes the time spent shopping for replacement property and planning the renovations. The SPE theoretically is the one making the renovations or at least paying for them.

Second, the construction or improvement exchange requires having “substantially the same property” that you identified by day 45 of the 1031 exchange timeline. The replacement property must end up with the same or greater value when it is deed back to the taxpayer. This approach allows you to buy a fixer-upper and make renovations within the 1031 exchange rules, but it requires careful project planning.

In theory, it allows you to buy land and build something, but that is not recommended due to the heavy tax bill you’ll face if you’re wrong. However, the like-kind rules are so liberal you could sell a rental house and buy a strip mall or sell raw land in an urban area and buy a ranch. However, if you sell property inside the United States, the replacement property must be within the U.S. as well.

Note that properties must be considered like-kind for the 1031 exchange to be approved. As a property investor, this means you can use a 1031 exchange to upgrade from a single-family home rental property to a triplex. And you can upgrade from the triplex to a 20 unit apartment building. There is no limit to how many times you do a 1031 exchange. Nor is there a limit to how frequently you do 1031 exchanges, only the time frame for the 1031 exchanges themselves.

You could avoid paying capital gains taxes as you continually roll over gains from one piece of property to another until you eventually sell for cash. What happens if you sell improved land (with buildings) for unimproved land? The depreciation for the buildings on the unimproved land may be recaptured as ordinary income and taxed as such, though you may avoid general capital gains. This is why you must have a professional guide you through this process.

Reverse 1031 Exchange

A reverse exchange can be described as buy first, exchange later. In this case, you’re buying the “replacement” or upgraded property first. Then you arrange for the sale of the second property. In the interim, the “relinquished” property is held by a Single Purpose Entity or SPE. Reverse exchanges are not very common, because they have to be all-cash deals. After all, you don’t have the equity from the first property available to pay for part or all of the second property.

Banks won’t lend you money for a reverse 1031 exchange. In contrast, they’ll be thrilled to loan you money to buy a stepped-up piece of property because of how much equity you’ll have in it. In a standard 1031 exchange, you run into problems if you have money but not the second property. With a reverse exchange, you’ll run into problems if you don’t relinquish the original property within 180 days.

However, the same time frames apply to a reverse exchange as the conventional 1031 exchange. You have 45 days to identify the “relinquished” property you’re going to sell and report it to the IRS. You have 180 total days to complete the sale and complete the reverse exchange with the replacement property.

When To Do a 1031 Exchange & Its Benefits?

The primary reason to execute a 1031 exchange is to reinvest capital into investments that are greater in scale, more diverse, or more aligned with your current investment strategy. And because taxes are deferred, more of the sale proceeds can be immediately directed toward your new investment. A 1031 tax-deferred exchange allows you to roll over money from a recently sold investment property into another property.

You’re able to defer capital gains taxes on the property’s sale. This tax rate will range from 15 to 30 percent. Suppose you own a rental house. Sell that property and use the money to buy two more rental houses. You’ve avoided a capital gains tax bill on the profit for that property, and you’ve used it to buy two more.

Section 1031 Exchanges offer a great opportunity to diversify assets, whether by diversifying into another geographic region or simply from one property type to another.

You can continue growing your portfolio over the years. You could continue to buy rental houses, or you could sell the properties and buy an apartment building. The 1031 exchange rules will let you roll the capital gains for 10 houses into a large multi-family project. You could in theory continue this until your death, potentially avoiding capital gains taxes until your estate has to deal with it.

Another benefit of a 1031 exchange is that it resets the depreciation clock. You’ll be able to buy a new property and take advantage of depreciation to offset your income. This can really add up if you’re selling a property that you’ve held for more than two decades. If you sell an investment property for more than its depreciated value, you will probably have to recapture the depreciation.

This normally results in the amount of depreciation included in your taxable income. A 1031 exchange avoids taxes on this amount that may exceed the official capital gains.

When do people want to do a 1031 property exchange?

The most common situation is when you want to avoid paying capital gains on the sale of a property. It may be done when you’re consolidating your real estate portfolio, selling multiple properties to invest in a single larger building. Or it may be done when you’re liquidating one property and investing in several more.

Also, if you have invested in properties that are low-income and high-maintenance, you could exchange the high-maintenance investment for a low-maintenance investment without needing to pay a significant amount of taxes. Or perhaps you want to move your investments from one location to another without the IRS knocking at your door.

Is 1031 Exchange Possible When There Are Losses Involved?

The goal of 1031 property exchanges is to avoid paying capital gains taxes on the sale of the property. In most cases, the 1031 exchange properties have a greater value than the one that was just sold. This may involve a more expensive home or a larger, multi-family unit. However, a 1031 exchange is possible when there are losses involved. Section 1031(b) specifically addresses cases where the transaction results in a loss.

The financial loss is not recognized at the time of the transaction. Instead, it is carried forward as part of a higher basis on the property you’ve received. Note that you can sell a property that you’re losing money on and roll the money into a new property as part of a 1031 exchange. The full benefit requires the replacement property to be of equal or greater value than the one you’re selling.

And if you’re selling a flooded house or property where the tenant isn’t paying the rent, almost anything you buy is a step up. If you are trading down in the property, you may get a “boot” in the form of debt reduction. Other forms of “boot” include prorated rent, utility escrow charges, service costs other than closing costs, and deposits transferred to the property buyer.

That money can be offset with cash used to purchase the replacement property. The boot used to include non-like-kind property including livestock, industrial equipment, and vehicles. This means you can’t count the value of animals on a farm or equipment in a factory towards either losses or gains in a 1031 exchange.

Consult with a tax professional to understand your options for avoiding a capital gains tax bill if you receive money like this. The Tax Cuts and Jobs Act of 2017 mitigated losses of 1031 exchanges by giving taxpayers the ability to immediately deduct certain expenditures. This might be classified as either a “bonus deprecation” or a business expense.

Here is An Example To Understand This Type of 1031 Exchange

Before you make any decisions, you must know the “adjusted basis” of your property. As the term implies, over time you adjust the basis in a property. If the “adjusted basis” is less than what the property is sold for, then we have a “total gain”. If the adjusted “tax basis” is more than what we sell the property for we have a true loss in the eyes of the IRS.

The adjusted basis is calculated by taking the original cost, adding the cost for improvements and related expenses, and subtracting any deductions taken for depreciation and depletion. Suppose you buy a $150,000 home. When determining the basis, start with this $150,000 and add any associated fees such as real estate taxes the seller owed that you paid as part of the transaction.

This figure is your basis. To get your adjusted basis, add or subtract any associated costs or credits. For example, if you invested $50,000 in home renovations, add this $50,000 to the basis to get an adjusted basis of $200,000. If you had storm damage to your home and had to pay $5,000 for roof repairs, add this amount to get an adjusted basis of $205,000.

If you do a 1031 exchange, all the total gain, including the tax on recaptured depreciation, will be deferred. If you exchange property with a true loss, then the loss amount is added to the basis of the replacement property. A simple example would be if you had a vacation area lot that cost us $200,000 that we sold for $100,000 and exchanged for a $100,000 lot close to your home.

You would have a $100,000 loss in the eyes of the IRS and would add your loss to the new basis of your replacement property. Because of the exchange, the new lot would have a starting basis of $200,000, even though you only paid $100,000 for the lot. While these rules are complicated, they must be followed—there are no exceptions or extensions. If you mess up, the IRS could decide you don’t qualify for a 1031 exchange and send you a huge tax bill. So make sure you know how it works. If you’re in doubt, consult an accountant or real estate agent for more details. For more information on 1031 exchanges, go to IRS.gov.

More Examples To Understand a 1031 Exchange Process

There are several initial steps to a successful 1031 exchange process. For example, you’ll want to find a qualified intermediary before you sell the property. Then there is the process of listing the property you want to sell. The first step in the 1031 exchange is selling the first property. It is advisable to have potential replacement properties identified at this point.

However, you don’t have to close on these properties immediately. If the 1031 exchange properties cannot be closed simultaneously, the money must be held by a qualified intermediary. This means the taxpayer doesn’t receive the money from the sale of the first property.

The second step in a 1031 exchange is formally identifying your replacement property. This must be done within 45 days of the sale date of the first property. Ideally, you’d have begun the purchase process.

The third step of the 1031 exchange process is to complete the purchase of the replacement process including payment and retitling of the property. The facilitator will hold the cash from the sale of the first property and send it to the seller of the replacement property. Then the 1031 exchange is treated as a swap by the IRS and considered done once you fill out the IRS form.

In general, you have 180 days from start to finish. However, you may have to do so even faster. For example, you generally have to complete the process before you file your tax return claiming the 1031 exchange. This means you’ll want to complete the 1031 exchange started last tax year before you file your tax return the following April.

If you actually acquire the replacement property before the first one sells, this is called a reverse exchange. The property must be held by an exchange accommodation titleholder. This could be a qualified intermediary. You’ll get the title transferred to you when the first property sells. What happens if there is money left-over after the new property has been purchased?

Maybe the new property costs less than you expected after all costs are taken into account. Or you didn’t use all of the money toward the purchase of a new property. A tax penalty will be owed, but it is typically only for the amount that wasn’t rolled over into the new property.

Let’s look at a few examples to understand what this means in practical terms. In the classic swap, you sell a rental property you bought for 150,000 dollars for 200,000 dollars and rollover the money into a 300,000 dollar duplex. While you’ll owe closing costs, legal fees, and a few other expenses out of pocket, you avoid paying capital gains taxes on the 50,000 profit. That would result in a 5,000 to 10,000 capital gains tax bill depending on where you live.

What happens if you have a property you’re going to take losses on? You bought a beach house at the peak of the market a decade ago for half a million dollars. You’ve maintained it but haven’t taken steps to increase its value. The area is in decline, so the property is only worth 400,000 dollars. Then you finally get a good offer. Someone is offering you 450,000 dollars for the property.

From your perspective, this is a loss. From the government’s perspective, you’ll owe taxes on the 50,000 gain including the recaptured depreciation. If you do a 1031 exchange when selling this property, the theoretical gain and recaptured depreciation are deferred.

1031 Exchange Rules That You Must Know

As an investor you can benefit from deferring the tax liability associated with the sale of real estate through a 1031 exchange. However, there are strict regulations and guidelines to be aware of that dictate what constitutes a valid exchange.

Several rules need to be followed while doing a 1031 exchange. Rules related to tax implications and time frames that may be problematic. If you’re considering a 1031 exchange, here is what you should know about all the rules.

If you decide to do a 1031 exchange, once the money from the sale of your first property comes through, it will be held in escrow—an independent account monitored by a third party. You won’t be able to access the money until you close on a new property. Note that you’re not allowed to use the money from the 1031 property exchange for anything else.

You can’t sell two commercial 1031 Exchange properties, do two quick fixes and flips and then roll the proceeds into a new apartment building. The money from the first transaction will be held by a qualified intermediary who acquires the replacement property for the taxpayer. And this is fine, provided you follow a few more rules.

Here are the important 1031 Exchange rules and regulations to be mindful of:

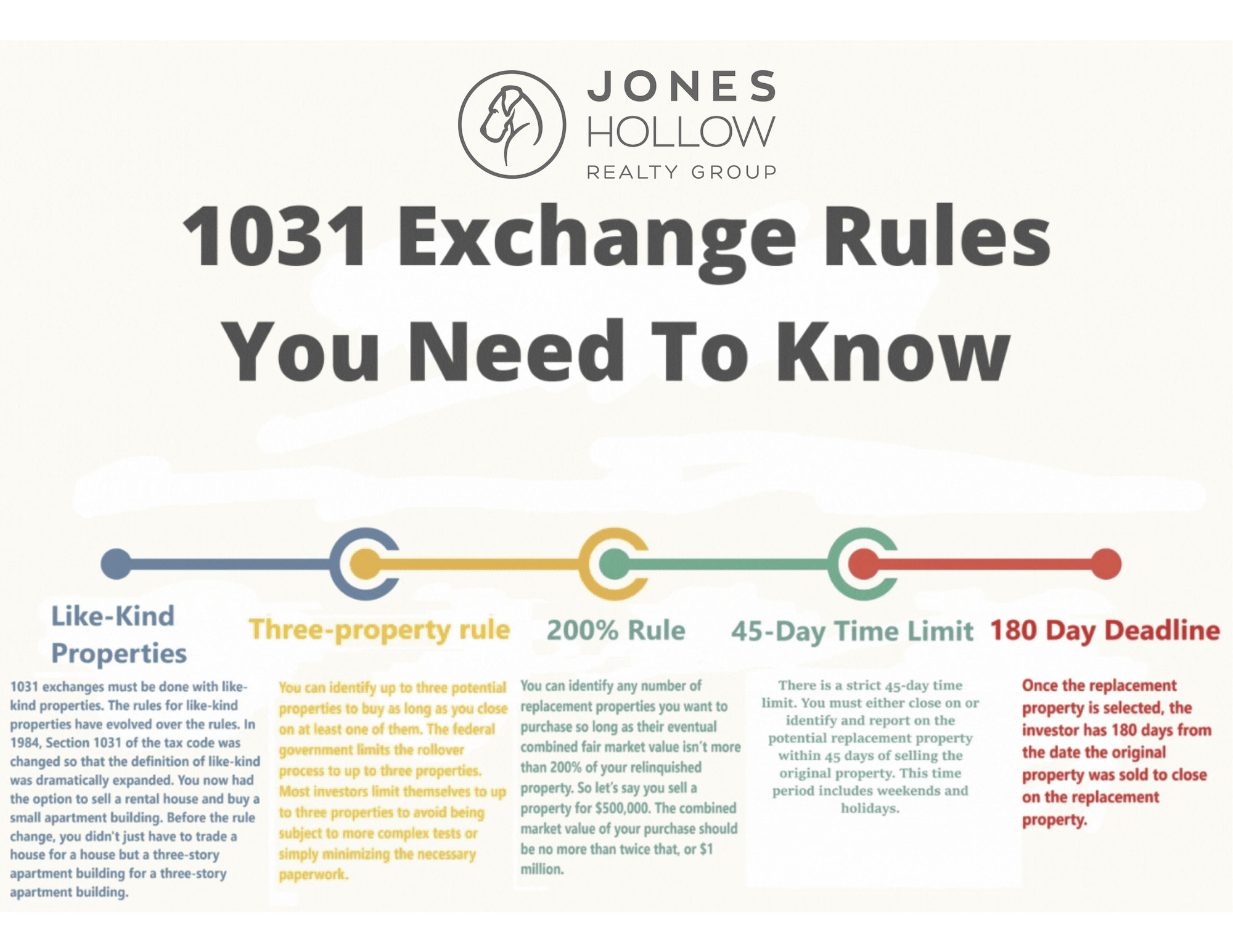

1. Like-kind Properties Rule

1031 exchanges must be done with like-kind properties. The rules for like-kind properties have evolved over the rules. In 1984, Section 1031 of the tax code was changed so that the definition of like-kind was dramatically expanded. You now had the option to sell a rental house and buy a small apartment building. Before the rule change, you didn’t just have to trade a house for a house but a three-story apartment building for a three-story apartment building.

The properties don’t have to be in the same sector. For example, you could sell an apartment building and invest the proceeds in an industrial building. International and domestic properties are not “like-kind” 1031 exchange properties, either. Yet you can use almost any property in the United States for a 1031 exchange. However, it is very important that if you cannot find the right property to reinvest the proceeds, don’t do a 1031 exchange. You should avoid buying the wrong property at the wrong time in the housing cycle.

2. Three-Property Rule

You can identify up to three potential properties to buy as long as you close on at least one of them. The federal government limits the rollover process to up to three properties. Most investors limit themselves to up to three properties to avoid being subject to more complex tests or simply minimizing the necessary paperwork.

3. 200% Rule

You can identify any number of replacement properties you want to purchase so long as their eventual combined fair market value isn’t more than 200% of your relinquished property. So let’s say you sell a property for $500,000. The combined market value of your purchase should be no more than twice that, or $1 million.

4. 95% Rule

You can ignore the 200% rule and identify any number of potential replacement properties for any amount as long as you buy 95% of the aggregate value of those properties. So if you sold a property for $500,000, you could identify five properties worth a total of $2,500,000. But you’d then have to actually buy at least $2,375,000 (that’s 95%) worth of those properties.

5. 45-Day Time Limit to Find a 1031 Exchange Property

The 1031 exchange used to have to be done nearly simultaneously. This caused a variety of problems because it can be hard to transfer titles and funds in a short period of time. However, the current 1031 exchange process still has a time limit. There is a strict 45-day time limit.

You must either close on or identify and report on the potential replacement property within 45 days of selling the original property. This time period includes weekends and holidays. If you pass that time limit, the entire exchange is disqualified. The IRS won’t interfere in the purchase of the new property. However, you’ll owe taxes on the sale of the old one.

6. 180 Days For the Transfer to Complete

After the sale, the clock starts ticking for you to find that new property: You have 45 days to identify a new property (or properties) you want to buy. Once the replacement property is selected, the investor has 180 days from the date the original property was sold to close on the replacement property. Since closing on a property can take time and is often unpredictable, many investors choose more than one property to buy with the hopes that at least one of them will come through.

7. Personal Residences Don’t Count as 1031 Exchange Properties

You can’t sell your personal residence and use part of the money to buy a rental. A general rule of thumb is that you can’t use a 1031 exchange if you lived in it for at least two of the past five years. Vacation homes and second homes typically don’t count, either. Paragraph 280 of section 1031 outlines the usage test that can be used to determine if a vacation home you rent out periodically can be included among 1031 Exchange properties.

8. Fix and Flip Properties Don’t Count as 1031 Exchange Properties

To qualify for a 1031 exchange, both the new and old properties have to be held as an investment or used in a trade or business. Held for investment means holding the property for future appreciation. Used in a trade or business means income-producing, such as used in a business or used as a rental property. A fix and flip kind of property is regarded as property held for sale. You may be able to count it as a 1031 exchange if you end up renting it out for a few months before selling it to an investor.

9. Land that you’re developing is not qualified for tax-deferred treatment under section 1031 of the tax code, though raw land might

A 1031 exchange can include build-to-suit exchanges, but the construction and property improvements must be completed by the 180-day time limit. In general, your interest in a partnership doesn’t count under section 1031. If you receive non-like-kind property like liabilities or cash equivalents, this could result in a tax bill. After 2018, the 1031 exchange could only include real property. Yet the exchange can include money such as proceeds after a mortgage is paid off.

Who Qualifies For a 1031 exchange?

Here are the basic requirements according to Los Angeles accountant Harlan Levinson:

The homes must be investment properties. This transaction is not for regular homeowners who live in the home they’re selling (or buying). Both homes in question must be investments, whether you plan to (or did) rent it out to tenants or flip it after renovations.

The home you buy must be worth more than the one you sell. People benefit from a 1031 exchange only when the property they buy is of equal or greater value than the one they’re selling—in other words, they’re trading up. For instance, maybe you bought a quaint summer cottage rental, but you want to cash that in for a larger mansion on the beach, or a duplex where you can rake in rental money from two families rather than one. If you intend to pay less for a new property, you’ll pay taxes on the difference.

How To Do A 1031 Exchange?

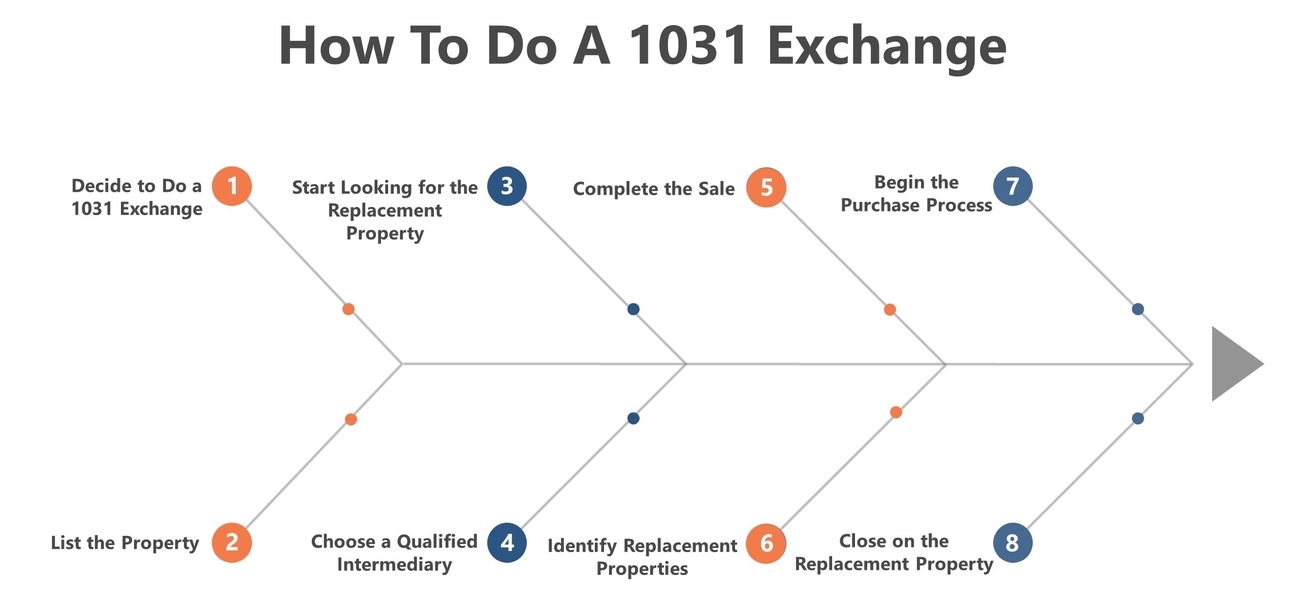

Step 1: Decide to Do a 1031 Exchange

Remember that not every real estate deal is suitable for a 1031 exchange. The IRS put strict limits on the use of the 1031 exchange on vacation properties. A 1031 exchange cannot involve your personal property or primary residence. This means you can’t use the 1031 exchange to eliminate the capital gains you may owe if you sell your family home for a significant profit. In theory, you can turn it into a rental and then exchange it, but the rules require you to meet very specific conditions, and we don’t recommend it. In practice, the 1031 exchange only applies to investment properties like apartment buildings or commercial real estate.

Step 2: List the Property

List the property for sale. You may want to include language in the listing paperwork that says you want to do a 1031 exchange. This informs them of the fact that you have deadlines to meet. And it saves you from dealing with people who stretch out the purchase process because they’re evaluating multiple properties.

Step 3: Start Looking for the Replacement Property

You could have identified several potential replacement properties after you decided to perform a 1031 exchange. However, you must formally identify one by day 45 after the relinquished property is sold. That’s why we recommend looking for the replacement property while the current one is up for sale. The typical replacement property costs somewhat more than the one you’re selling, because you may owe capital gains taxes if you end up keeping some of the proceeds of the property sale.

Step 4: Choose a Qualified Intermediary

You need a qualified intermediary in place to receive the money from the sale of property 1 before you can buy property 2 under the 1031 exchange. Only work with a professional experienced with 1031 exchanges. IRS laws explicitly state that you are not allowed to use your own attorney, employee, accountant, real estate agent, or a relative as the qualified intermediary. What is the qualified intermediary’s role? If they receive the profits from the sale and roll it over into a new property, you never received the money. And you probably can’t be charged income tax or capital gains taxes on it.

Step 5: Complete the Sale.

The purchase agreement the buyer signs must clearly state that a 1031 exchange is taking place. This information will affect everything from assignments to disclosures. Like standard real estate deals, you’ll have a title company and/or lawyer involved in the closing. Unlike other real estate transactions, the money from the sale will be transferred into the qualified intermediary’s bank account, not yours.

Step 6: Identify Replacement Properties

You can identify up to three replacement properties within 45 days. The IRS gets notified via IRS Form 8824. You can in theory close on more properties if you close on at least 95 percent of them or the identified properties have a combined value of less than 200 percent of the sold property. In this regard, you could sell a 500,000 dollar house and buy four 250,000 dollar houses.

You’ve bought smaller properties, but you still get to take advantage of the 1031 exchange because it has a higher total dollar value than what you sold. Most 1031 exchanges involve buying a property that is a step up. By identifying several replacement properties such as apartment buildings, you ensure that you remain within the rules if your first choice falls through.

Step 7: Begin the Purchase Process

Sign a contract for your identified properties. We’d recommend having contingency clauses that let you back out on the other properties if the first deal goes through. Negotiate the purchase of the property, while your qualified intermediary works with the title company. An experienced intermediary is familiar with it.

Step 8: Close on the Replacement Property

When you close on the replacement property, the intermediary sends your money to the seller’s attorney or their title company. The closing process will then proceed like any other. Yet you’ve avoided the associated capital gains taxes.

Conclusion

A 1031 exchange allows real estate investors to grow their wealth more quickly because they avoid a hefty tax bill every time they reinvest the proceeds of a property sale. That is why it is a powerful tool for those who want to grow their portfolio. The savings of the 1031 exchange are so substantial that it is used by businesses and real estate investors alike to save money. The biggest reasons why people don’t take advantage of them are because they either want to reduce their exposure to real estate or can’t find a good replacement property in time.

So, next time you decide to do a a 1031 exchange, you must to keep in mind all these things to complete the process successfully.